Fintech Onboarding UX: What Stripe, Wise, Revolut, Robinhood, and Mercury Get Right (And Wrong)

We analyzed the onboarding flows of Stripe, Wise, Revolut, Robinhood, and Mercury — user reviews, real drop-off data, and design patterns. Here's what actually works and where each product fails.

Key takeaways

- Fintech onboarding fails most after KYC approval: 40% of Robinhood users went inactive right after first funding.

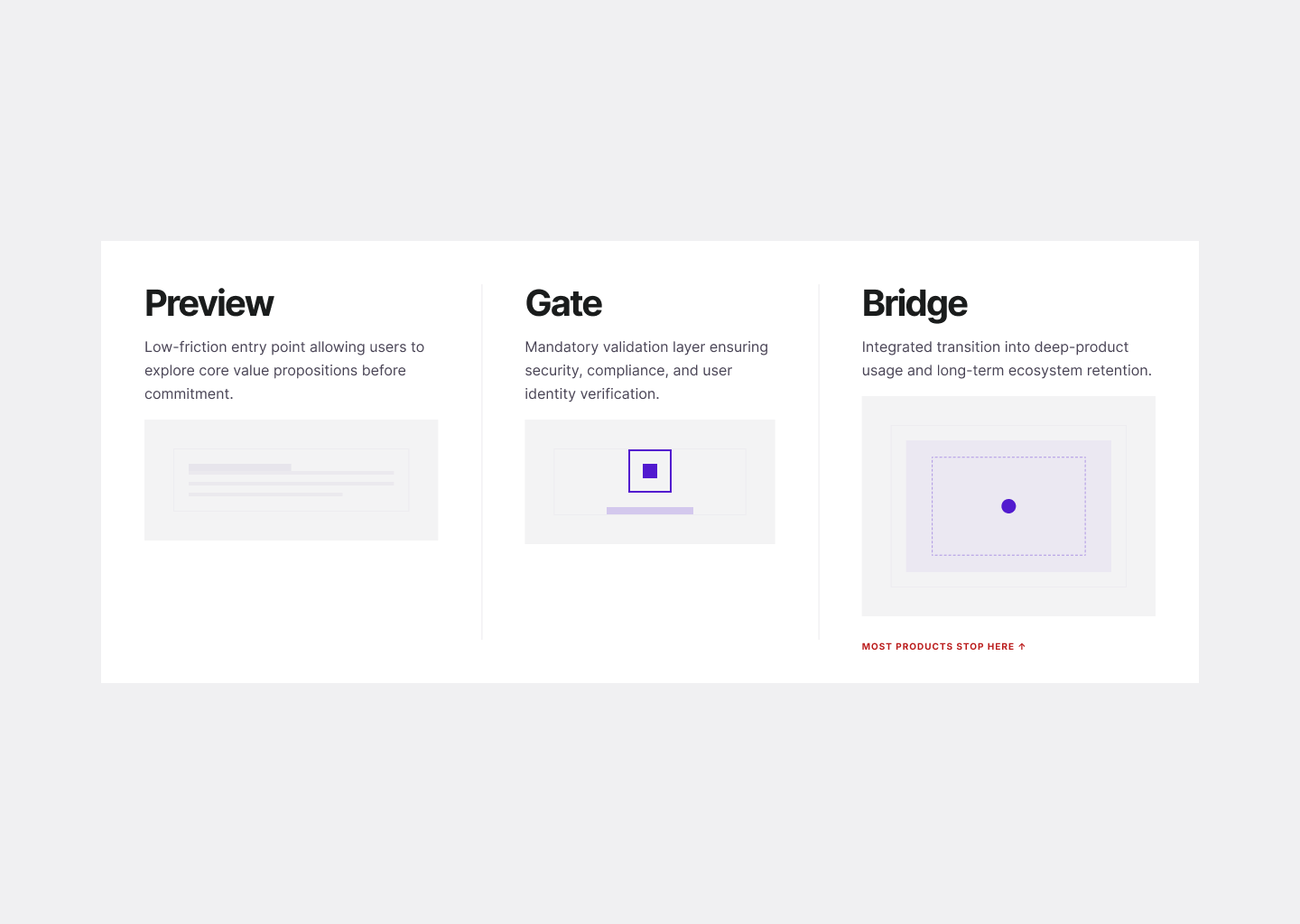

- Treat onboarding as three phases — Preview, Gate, Bridge — and design the Bridge activation gap nobody optimizes.

- Show core value before signup; Wise's unauthenticated rate calculator and Robinhood's demo trade turn signup into a logical next step.

- Name the KYC rejection category and offer a retry path — generic 'try again tomorrow' is the top abandonment trigger.

The Drop-Off Nobody Talks About

Fintech onboarding gets a lot of design attention. Every product team measures signup completion, tracks document upload rates, A/B tests button copy. The conversion funnel from "land on homepage" to "account created" is usually well-instrumented and actively optimized.

The problem is that this is the wrong funnel to optimize.

The real drop-off doesn't happen at the selfie page or the address field. It happens after verification — when the user has been approved, landed inside the product, and has no idea what to do next. Robinhood's own data is the clearest evidence: 40% of users became entirely inactive immediately after their first account funding step. They got through the whole flow, funded the account, and stopped. The product treated funding as the finish line. Users treated it as an entrance they didn't know how to navigate.

This pattern is consistent across all five products we analyzed. Different strengths, different user bases — but the same structural blind spot: onboarding is designed as a compliance exercise, not a product experience.

Three Phases That Actually Matter

Fintech onboarding isn't one flow. It's three distinct experiences, each requiring different UX thinking:

Phase 1 — Preview: Before a user hands over their email, they're forming a belief: is this product worth the effort of signing up? Most fintech products skip this phase entirely and open with a signup form.

Phase 2 — Gate: Identity verification (KYC) is legally mandatory and unavoidably friction-heavy. The design question isn't how to eliminate it — it's how to make it feel purposeful rather than punitive. The difference between a product that communicates clearly and one that just spins a loader is the difference between a user who waits and one who abandons.

Phase 3 — Bridge: The activation gap. The moment between "you're approved" and "you just did something meaningful." This is where fintech onboarding most commonly fails, and where the most valuable design work goes untouched.

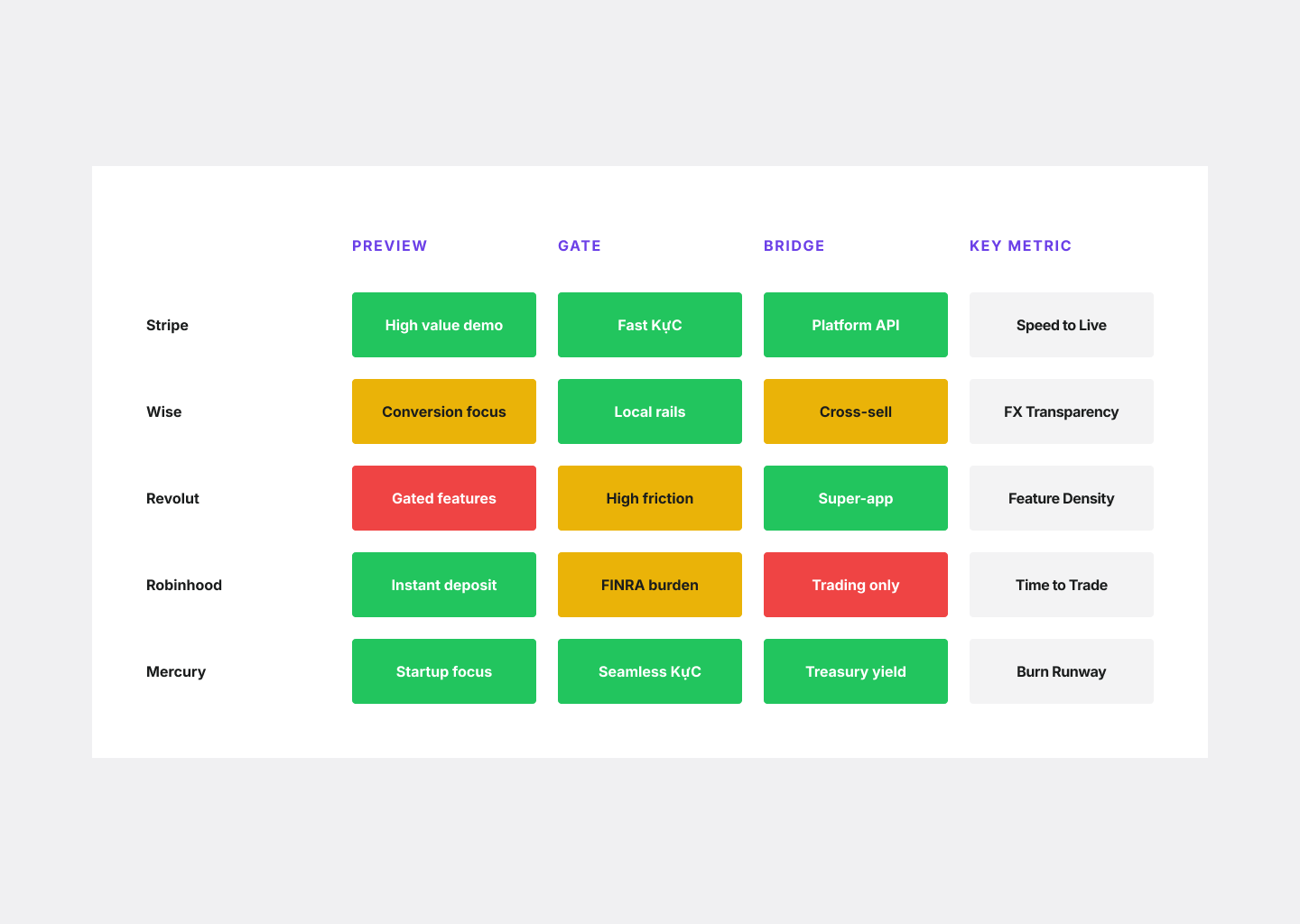

This is the Masterly Fintech Onboarding Model: Preview → Gate → Bridge. Each product we analyzed does at least one of these well. The ones that do all three retain users.

Stripe

Who it's for: Developers building payment infrastructure, and non-technical business owners and CFOs managing merchant accounts.

Phase 1 — Preview: Stripe skips it for consumers but gets it right for developers. API keys and a functional sandbox are available within seconds of entering an email — no business verification required to start building. For Stripe Atlas users, the pitch is concrete: 90% of founders are ready to fundraise, open a bank account, and charge customers within two business days of submitting their application.

Phase 2 — Gate: Highly variable — and that variability is Stripe's biggest UX problem. Standard merchant onboarding is smooth: progress bar, inline validation, localized for all supported countries, three configurable modes (hosted, embedded, API). Advanced products — Stripe Issuing, Treasury — become multi-week compliance projects. More critically, default risk settings can silently block features like ACH processing without explaining why, forcing users to find the right toggle after the fact. Trustpilot reviews consistently describe accounts working fine until the first real transaction, then a hold with no explanation.

Phase 3 — Bridge: Stripe's biggest advantage here is networked onboarding. Serial entrepreneurs with an existing account can port verified business details to a new account instantly. For first-time users, no equivalent shortcut exists.

Stripe's Connect Express redesign produced an average 5.3% lift in onboarding conversion, with one platform reporting 17%.

Gets right: Dual-audience design — developer speed and business-owner clarity without degrading either. Gets wrong: Post-KYC silent failures that surface only after a user has invested trust and started processing payments.

Wise

Who it's for: Individuals and businesses moving money across borders. Trustpilot aggregate: 4.3/5 from over 290,000 reviews — broadly positive, with a concentrated negative cluster around verification loops.

Phase 1 — Preview: Wise's strongest phase, and one of the best examples of value-before-auth in fintech. The homepage exchange rate calculator is functional and unauthenticated — users see the actual mid-market rate and exact fee before creating an account. Built for Mars' teardown identifies this as a key conversion driver: by the time a user enters their email, they've already made a purchase decision based on real numbers, not marketing claims.

Phase 2 — Gate: For standard personal accounts, fast — under 10 minutes for most cases. The product shows estimated time at each step and allows save-and-resume across devices. Where it breaks down: KYC session links expire in five minutes per Wise's own developer documentation — short windows that interrupt users on slow networks or mid-device-switch. Regional compliance can stack multiple verification layers with no indication of what's required until mid-flow. The dominant 1-star pattern on Trustpilot: "Locked my account, asked repeatedly for the same documents I was submitting each time."

Phase 3 — Bridge: Once verified, the core action — initiating a transfer — is immediately accessible and well-guided. The joint account flow is a notable gap, triggering manual verification friction the primary flow avoids.

Gets right: Radical transparency on pricing. Time disclosure at each KYC step. Cross-device resumability. Gets wrong: Five-minute session link expiry, opaque rejection messages, and a support system that fails exactly when users are most anxious.

Revolut

Who it's for: Mobile-first consumers in Europe wanting a multi-currency account. Trustpilot: 4.7/5 from over 406,000 reviews — highest of the five, with 80% five-star. The negative cluster is concentrated around post-onboarding account freezes.

Phase 1 — Preview: The weakest phase. Revolut leads with tier comparison — Standard vs. Plus vs. Premium vs. Metal — before the user has any basis for evaluating the differences. The product asks for a commitment decision before establishing any value.

Phase 2 — Gate: Where Revolut wins decisively for eligible users. By partnering with GBG for electronic identity verification, Revolut reduced time to pass KYC from approximately 70 minutes to approximately 2 minutes for eligible UK customers — a 97% reduction that delivered a 12% net increase in global onboarding completions. When eIDV passes, no document upload is ever required.

The fall-back breaks this. Users whose identity doesn't match data bureau records drop to document upload plus selfie, extending to five business days. The selfie page generates 11% drop-off; the subscription selection page generates 13% drop-off — users forced to choose a paid tier before establishing any trust in the product. That's 24% of high-intent users lost at two specific, knowable, fixable points.

Phase 3 — Bridge: Aggressive upsell immediately after onboarding undermines the experience Revolut just built. Before the user has done anything useful, they're pushed toward Premium tiers. Upsell works after value delivery, not before it.

Gets right: Best consumer KYC speed in the category. App-only signup. Multi-currency wallet usable instantly post-KYC. Gets wrong: Tier selection before value delivery, and "security review" freezes with no explanation — the dominant complaint in the 7% of negative Trustpilot reviews.

Robinhood

Who it's for: Retail investors in the US, mobile-first and new to investing. Over half of customers who funded accounts between 2015 and 2021 reported Robinhood was their first brokerage account — that's the ICP in one sentence.

Phase 1 — Preview: The strongest preview phase of the five. Robinhood lets users build a watchlist and simulate a trade before SSN is required — before any sensitive data is collected at all. The three-CTA structure at entry (Register / Learn More / Try Demo) reduces decision anxiety by giving hesitant users an exploration path that doesn't feel like rejection.

Phase 2 — Gate: Clean and fast — 16 clicks, 11 fields, with Plaid handling bank linking automatically. SIPC protection ($500,000) surfaces alongside bank linkage — the right trust signal at the right moment. Where it fails: when ID verification fails — from poor photo quality, an SSN typo, or a duplicate account — the response is "try again tomorrow" with no explanation of what went wrong.

Phase 3 — Bridge: The most instructive example in the category, in both failure and recovery. Original failure: 40% of users became inactive immediately after first account funding. The fix: Robinhood integrated Pinwheel's PreMatch technology to automatically detect active payroll accounts after MFA — eliminating the manual employer lookup that preceded direct deposit setup. Direct deposit conversion doubled.

Gets right: Best pre-auth exploration of the five. Automated payroll detection that closes the activation gap. Gamified first-trade confetti — the canonical aha moment. Gets wrong: Generic rejection errors, and immediate promotion of margin and options to users who've never invested before.

Mercury

Who it's for: Startups and founders who need a business bank account without visiting a branch. Trustpilot: 4.0/5 from 2,500+ reviews. NPS of 75, compared to a banking industry average of 34.

Phase 1 — Preview: Mercury relies on reputation rather than in-product preview. Word of mouth from the founder community does the acquisition work. For founders outside the core ICP (US-incorporated startups), there's no equivalent of Wise's calculator or Robinhood's demo to anchor the decision.

Phase 2 — Gate: Mercury's most impressive design work. The application is split into two phases: basic credentials first (~5 fields), then formal business documentation. Phase 1 data lets Mercury recover abandoned signups — if a founder drops off during document collection, the contact info is already in the system. For document processing, Mercury deployed real-time parsing achieving 98% accuracy on edge cases with 5–7 second feedback cycles. If a founder uploads a blurry image or the wrong document, they know immediately — not after 48 hours.

Phase 3 — Bridge: An explicit post-approval status tracker shows what Mercury is reviewing and what the founder can do in the meantime. Zero upsell pressure — no pre-checked paid tier boxes anywhere in the flow. The gap: Mercury support is M–F, 6am–5pm PT only. If KYC needs human review on a weekend, nothing moves.

Gets right: Two-phase structure. Real-time document validation. Transparent wait-state communication. Zero onboarding upsell. Gets wrong: Application denials without explanation for non-standard entities, and weekend support gaps.

The Masterly Fintech Onboarding Model

Preview is where Wise and Robinhood win. Show core value before asking for anything — a fee calculator, a demo, a rate comparison. The signup that follows feels like a logical next step, not a gate.

Gate is where Mercury and Revolut (when eIDV works) win. KYC is unavoidable, but it can be transparent and fast. Revolut's 97% KYC time reduction is the consumer benchmark. Mercury's two-phase split with real-time document feedback is the B2B benchmark.

Bridge is where nobody fully wins yet. The activation gap between approval and first meaningful action is the most underdeveloped phase across the entire category. The question isn't only "how do we reduce steps to first deposit" — it's "what does the user need to understand and do in the first 10 minutes of having an active account?"

One strategic choice shapes everything else: speed or trust signals — pick one. Revolut's 2-minute promise inherently means lighter AML screening for some users. Mercury's 1–2 day approval window inherently means slower time to aha. Neither is wrong. Both require messaging built honestly around the tradeoff.

| Product | Preview | Gate (KYC) | Bridge (Activation) | Standout Metric |

|---|---|---|---|---|

| Stripe | ✅ Instant sandbox for developers | ⚠️ Silent post-KYC blocks on first transaction | ✅ Networked onboarding for returning users | +5.3% conversion via Connect Express (up to +17%) |

| Wise | ✅ Unauthenticated rate calculator | ⚠️ 5-min link expiry; opaque rejection messages | ✅ Clear first-transfer action post-approval | 4.3/5 Trustpilot (290k+ reviews) |

| Revolut | ❌ Tier selection before value established | ✅ 97% KYC time reduction (70 min → 2 min via eIDV) | ❌ Upsell pressure before first value delivery | 4.7/5 Trustpilot (406k+ reviews) |

| Robinhood | ✅ Watchlist + demo trade before SSN | ⚠️ Generic "try again tomorrow" on rejection | ✅ Payroll auto-detection 2× deposit conversion | 16 clicks, 11 fields; 40% post-funding inactivity (fixed) |

| Mercury | ⚠️ Relies on reputation, no in-product hook | ✅ 5–7s real-time doc validation; two-phase split | ✅ Transparent review timeline; zero upsell | NPS 75 vs. banking industry average 34 |

Four Mistakes That Are Costing You Activations

1. Treating KYC completion as the conversion goal

KYC approval is not activation. A user who has verified their identity but hasn't made a transfer, funded an account, or completed a transaction hasn't experienced the product's value. Robinhood's 40% post-funding inactivity exists precisely because the product treated funding as the finish line.

2. Using generic rejection screens

When KYC fails, most products tell users to "try again tomorrow" with no explanation of what went wrong. The fix: tell the user the category of failure — image quality, name mismatch, document expired — and offer a one-tap retry path. This is the most commonly cited abandonment trigger across App Store reviews for Robinhood and the dominant 1-star pattern for Wise on Trustpilot.

3. Upselling before delivering

Revolut's subscription selection page generates 13% drop-off — users asked to choose a paid tier before they've experienced the free one. Upsell belongs after the first value moment. Mercury's decision to keep onboarding free of upsell pressure is part of why its NPS is 75.

4. Not designing the waiting period

KYC review, bank verification, and compliance checks all involve waiting. Most products communicate this with a generic "we'll email you" and go silent. Mercury's pending-review screen is the better model: tell users what step they're on, what's being reviewed, what they can do while they wait. Users who don't know what's happening assume something is wrong.

Onboarding Design Checklist

| Question | Why It Matters |

|---|---|

| Can a user experience core product value before entering personal data? | Value before auth reduces signup anxiety and improves commitment quality |

| Do you run electronic identity verification before requiring document upload? | eIDV-first can reduce KYC time by 97% (Revolut benchmark); documents only as fallback |

| Is signup split into two phases — low-friction first, documents second? | Phase 1 data enables recovery of users who drop off during document collection |

| Do rejection states name the category of failure and offer a retry path? | Generic "try again" messages are the #1 KYC abandonment driver across all five products |

| Is the verification wait state designed — not just acknowledged? | Users who don't know what's happening assume something is wrong |

| What is the user's first action after KYC approval? | If there's no designed path from approved to active, the activation gap is already a retention problem |

| Is upsell deferred until after first value delivery? | Subscription pressure before first use trains users to distrust the product |

If Your Onboarding Has an Activation Gap

The patterns across these five products converge on the same problem: most fintech onboarding has been optimized through KYC and stops there. The transition from verified to active — the Bridge phase — is where the most significant retention work still lives.

A UX audit of a fintech onboarding flow typically surfaces the drop-off at a predictable moment: not the selfie page, not the address field, but the screen that appears after approval. The one that says "you're all set." It rarely is.

If your activation rate is more than 20 percentage points below your KYC completion rate, the gap is in Phase 3 — and it's almost certainly undesigned. Masterly works with fintech companies at Series A–D to audit and redesign onboarding flows, including the activation phase that most optimization efforts never reach.

View our fintech design work or learn about our UX audit service.